P2P (Peer to Peer)

Imagine applying for a loan, simply by providing a few data points on an online fintech portal, and within few mins/hours having your loan approved for funding; as against the traditional process of visiting the Bank / NBFC branch; which typically takes an average waiting period of 2-3 days to approve a credit line/loan. Globally, on account of technological disruption, a number of online Fintech marketplaces have made this a reality and are offering online platforms that match borrowers directly with investors/lenders. This concept of connecting lenders with borrowers directly via an online market place with enhanced transparency is called peer-to-peer (P2P); or marketplace lending model. These models are growing in popularity amongst borrowers because of its perceived low interest rate, simplified application process and quick lending decisions. In particular, P2P platforms seem to have found a niche by offering borrowers an improved lending experience and they are quickly gaining momentum.

What is Peer to Peer (P2P) Lending:

Peer-to-peer lending, also abbreviated as P2P lending, is the practice of lending money to individuals or businesses through online services that match lenders with borrowers without the intermediation of traditional financial institutions (Banks / NBFCs). The development of advanced financial technologies, or fintech, by integrating banking processes with information technology has enabled the creation of financial products and services that can be delivered to consumers at scale, and at a fraction of the cost incurred by conventional banks and NBFCs. Since P2P lending companies operate online, they can run with lower overheads and provide the service more cost-efficiently than traditional financial institutions. Thereby creating a win-win ecosystem, where lenders can earn higher returns compared to savings and investment products offered by banks, while borrowers can borrow money at lower interest rates.

Indian P2P Landscape:

P2P lending service providers have been in business in India since early 2012, but there were no regulations around it until Sept 2017. In Sep 2017, RBI notified that these service providers need to be registered as non-banking financial companies (NBFCs – P2P) and came out with guidelines and licensing norms for P2P lending platforms in Oct 2017.

About P2P

P2P is an RBI regulated entity registered as Peer to Peer Lending platform uses new-age technology to match prime borrowers and lenders and in the process eliminates the high intermediation cost plus margins charged by traditional banks and NBFCs, thus, making borrowing cheaper and investing/lending a more lucrative opportunity as compared to traditional investment avenues.

Key Focus Areas to Source Borrowers:

- Upskilling Education Financing

- Discretionary Healthcare Financing

- Home Improvement Financing

What Sets P2P Apart:

No interest charged to the Customer; income is earned from the Dealers Margin through subvention. Rather than paying the complete amount upfront, the customer pays 20-30% as down-payment & balance is re-paid in over average 7-9 months without additional cost

Focusing on only selected segments: Education, Healthcare and Home Improvement which have a very strong end-use case and lesser chances of default – Monies get disbursed to the dealer and not to the borrower

Through their tie-ups; they are able to attract quality borrowers who are not credited hungry in the first place and thus have a higher intent of repaying the loans

Getting borrowers from select sources gives them better insights for underwriting and pricing them. They are able to assign weightages to demographic, end-use case, past repayment history and accordingly rate the borrowers

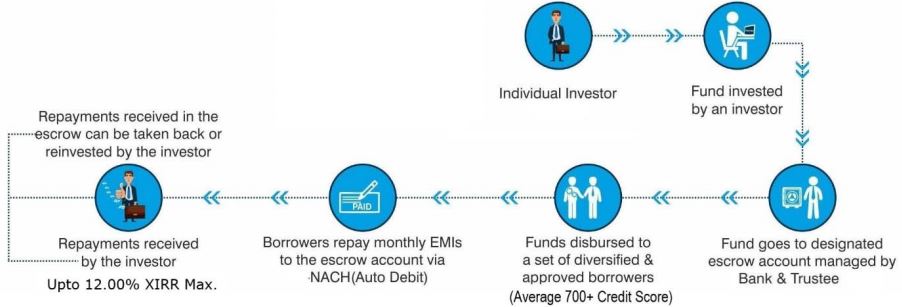

Lending Process:

P2P lends to high quality (prime) borrowers located in Tier I & Tier II cities, largely salaried individuals with an average salary of 25k per month.

LiquiLoans has tied up with various Healthcare & Education dealer partners; where customers who visit such stores are offered Zero Cost EMIs to avail the services (Subject to details like PAN, DOB, Address, Employment Details, Loan Requirement & Access to Credit Bureau Reports is provided by the borrower via the online dashboard & then such profiles are evaluated and either approved/disapproved by LiquiLoan’s Credit Team). Each dealer is trained on the entire loan process.

LiquiLoans provides a Zero Cost EMI option to the approved customers at the point of sale.

The Bureau report of the borrower is exhaustively analyzed. Cases with credit bureau scores lower than 600 are directly rejected.

Liquiloans have a strong underwriting mechanism, whereby they assess the borrowers’ Credit report in detail; which helps them get detailed information about the customer’s past borrowings/payment history (delays/defaults, if any). They do a thorough check on the borrowers current & previous employment status and longevity of borrower’s service at a particular organization. Additionally, they also have multiple other checks like evaluating past 6 months’ bank statements / previously filed ITRs etc.

Liquiloans sends an E-Loan Agreement to customer/borrower which is digitally signed using email OTP. NACH (Auto–debit mandates) are mandatorily signed by the customer/borrower at the store itself.

Once signatures are done, ops team cross checks the KYC, Address Proof, NACHs & E-Agreements.

Once signed loan agreements, NACH and requisite supporting docs are found in order, the loan is disbursed directly to the dealer account after deducting subvention. Funds are routed through the IDBI Escrow Account.

To ensure monthly EMI deductions from the customer’s bank account; each NACH is duly registered. This NACH is also scanned into the LOS and automatically filled by their systems without any manual intervention.

SMS, Email, Telephonic reminders are sent to ensure that customers maintain sufficient balances before their EMI due date. In case of any delay in loan, experienced team of Tele-callers follow up with borrowers and take the process forward.

An internal recovery team pursues these cases from day 1 and for delays that have crossed a period of 90+ days; is given to one of their recovery agencies to pursue. Liquiloans has a PAN India & region-specific tie-ups with agencies that help in recovery.

Product Characteristics – Enhanced Safety:

- RBI Regulated & Monitored Product: Monies flow only through an Escrow Account (PSU Bank) & Managed by a Bank Sponsored Trustee

- Alignment of Interest: No Income/Fee shall be earned by P2P till the Investor / Lender gets back the principal plus the indicative return

- Average Loan Tenor: <12 Months

- Average Loan Size: ~INR. 50-75k (Which is an Avg. 15-25% of Borrowers Annual Salary)

- Multi-fold Diversification: Avg. Exposure per Borrower shall be < 1% of the overall portfolio; Avg. 100-300 Borrowers are assigned to each Lender

- Payout Options: Monthly Interest Payout / Auto-Reinvestment Option

Key Dealers Partners: P2P has partnered with leading dealers such as Dr. Batra, Richfeel, Morpheus IVF, QuantInsti, Great Lakes, Lifecell etc. for sourcing prime quality, creditworthy borrowers on the platform. Liquiloan’s partners are amongst the largest in their respective fields; such as IVF treatments, Stem Cell Banking, Online Education Courses, Hair & Skin Treatments, Quant-Trading Courses etc.

Risk and Mitigation

- Credit Risk: Present default rates in Fintech lending segment is anywhere between avg. 2%-7%. Credit risk is eliminated given the nature of Prime Borrowers (Avg. 700+ Credit Bureau Scores) & Zero cost EMI loans sourced through Liquiloan’s platform backed with strong underwriting mechanisms.

- Re-Investment Risk: Currently, all P2P Platforms take an average of 3-15 days to redeploy the funds. P2P tries to mitigate this risk by increasing the diversity of dealers and borrowers by reaching out to different profiles across multiple cities.

- Yield to Maturity Risk: The investment returns are primarily not linked to market interest rate movements and hence remain unaffected by interest rate changes.

- Concentration Risk: Granular diversification between 100-300 borrowers ensures that at no point does one borrower contribute to a large part of the lender’s portfolio, thereby mitigating concentration risk at an account level.

Conclusion

Fintech Platform-based lending will invariably gain huge momentum over the next three to five years due to their competitive interest rates and ease of making finance available. P2P is a unique model as it is predominantly an online business in which individuals and institutional investors provide funding to retail borrowers seeking loans. The market for P2P lending is anticipated to benefit from the strict credit policies implemented by financial institutions. With faster approval rates and simplified processes; ease of lending and borrowing is set to drive the market.

The investment opportunity in P2P is similar to a debt mutual fund where your investment is diversified across multiple borrowers and managed by experts. The exposure is towards small-ticket retail consumer loans which is generally considered safer than corporate debt. On account of lower cost & elimination of middlemen, the returns can be up to 1.5x-2x of liquid debt mutual funds. P2P is set apart from other P2P players as it focuses on only selected segments, education, healthcare & home improvement, which have very strong end-use cases and limited chances of default.